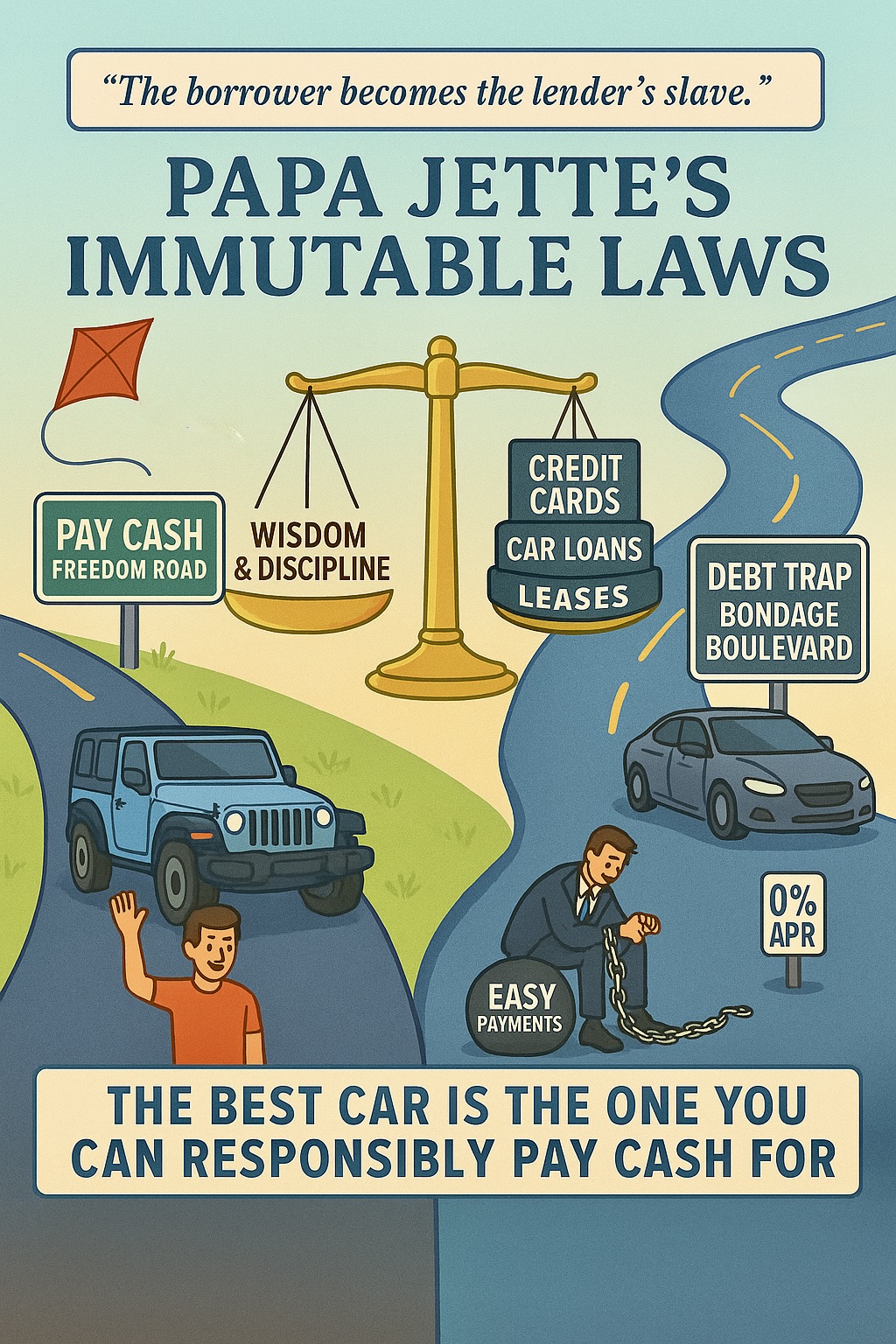

“The rich rules over the poor, and the borrower becomes the lender’s slave.“ Proverbs 22:7 (NASB)

Our grandson paid cash for his first car. Hurray! He bought a used Jeep. Ugh. 😟

He’s transitioning from HVAC school to his first full-time job and recently called to ask for help. He wants to buy a different car and is exploring his options. At twenty years old with a decent-paying job, he’s tempted by those easy monthly installments—time to earn my Grandpa stripes.

Living in a place like the United States, taking certain things for granted, like food, shelter, clothing, and transportation, is easy. These are the building blocks of human flourishing. A key part of that flourishing is our access to capital, an economic engine that has improved lives.

But access to capital without wisdom is dangerous. Borrowing money responsibly requires discipline. And credit cards, car loans, and leases? They demand the most.

🚗 “No money down, no payments for 90 days, and 0% APR for qualified buyers!”

Sounds like a dream. Here’s the reality, buried in the fine print:

- 0% APR only applies to top-tier credit scores.

- The price of the car may be inflated to offset the “deal.”

- No payments for 90 days doesn’t mean interest isn’t accruing—it’s just deferred and tacked on later.

- Loan terms are often extended to 72–84 months, putting buyers underwater and on the hook long after the new-car smell fades.

And leasing?

🚘 Leasing: The Never-Ending Bill

Sure, leasing looks affordable month-to-month. But over time:

- You’re always making payments.

- You never build equity.

- You may pay more than if you’d bought and kept a slightly used car.

On top of that, leases come with:

- Acquisition fees

- Disposition fees when the lease ends

- Early termination penalties if you want out early

The contracts are complicated, and—surprise—the dealership wins..

It’s delayed pain dressed up as a wise decision. They’re selling you a depreciating asset you often can’t afford and framing it like it’s barely a financial decision at all.

Those “easy payments”? They become chains.

If you’ve been making car payments for a while… can I get an “Amen”?

🔐 Papa Jette’s Immutable Laws

On car purchases: After doing your homework, the best car you can buy is the one you can responsibly pay cash for.

On credit cards: Only use one if you have the wisdom and self-discipline to follow a budget. Never, ever carry a balance.

💡 Access to capital is a powerful tool for flourishing. But it is also risky because it is always a presumption on an unknowable future.

Run the Play: Follow Papa Jette’s immutable laws. Your future self will thank you. 😀

💬 Finding Our Place in the Story

Am I currently using debt as a tool for wise stewardship—or as a shortcut to get something I want before I can afford it?

(What is my true motivation behind borrowing money?)

What would change in my life—financially, emotionally, spiritually—if I committed to living debt-free going forward?

(How might freedom from monthly payments open doors to generosity or peace?)

Have I ever mistaken easy payments for affordability?

(What past financial decisions taught me the most about the long-term cost of “deals” that seemed too good to be true?)

Leave a Reply